First, let's take a look at one of the most discussed anomalies of late, the different paths of the S&P 500 and ten year note yields. Treasury yields tend to move in tandem with equity prices when market money flows are 'normal', that is when money leaves the safety of treasuries and finds its way into equities. Notice in the chart below, however, that the ten year yield has moved lower (money is flowing into treasuries) while equities have moved higher. Yields typically drop during periods of risk aversion, or when investors move away from risk. The drop in yields along with the very low overall volume shows that the recent move may have just been HFT shops and quant traders merely recycling existing funds in equities instead of equities benefiting from solid money flows from 'safer' asset classes to fuel rallies. We saw the same situation in April 2010, just before equities peaked.

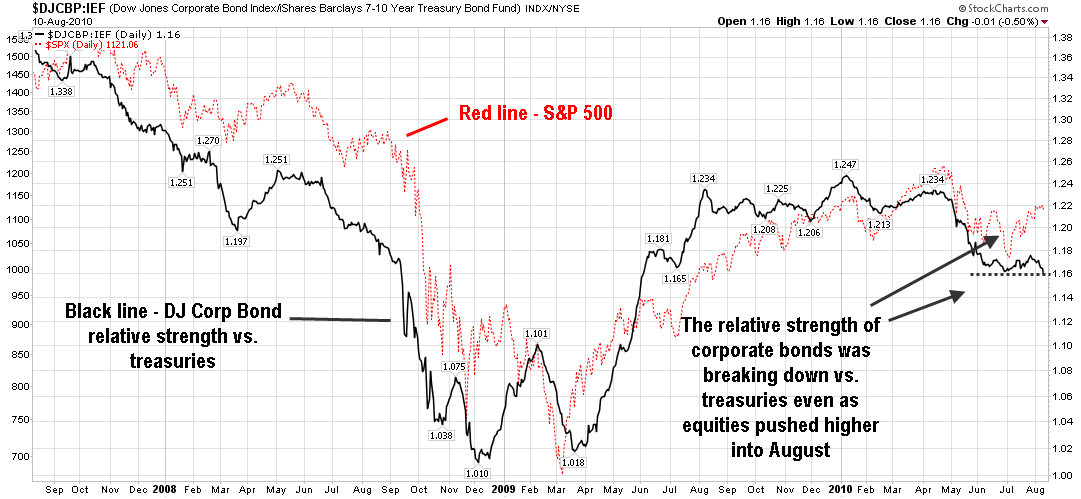

Next, let's take a look at one of my favorite risk measurements - corporate bonds vs. treasuries. As investors feel better about economic growth prospects, they tend to move out into corporate bonds and away from treasuries. This typically provides higher yield which is a reward for higher risk exposure. While the yield spreads between corporate bonds and treasuries have narrowed, corporate still provide a higher yield, but investors are embracing treasuries as their first choice. In the chart below, the black line is a relative strength line between corporate bonds (the Dow Jones Corporate Bond Index), and IEF (the 7-10 year treasury ETF). When the black line is rising, corporate bonds are seeing higher inflows than treasuries. When the black line is falling, treasuries are seeing higher inflows that corporates. The red line is a plot of the S&P 500.

Notice how the two lines tend to track well together, meaning that when investors take on more risk in the bond market, it is also good for equities. Recently, however, the relative strength of corporate bonds has broken down vs. treasuries, showing once again that investors are not embracing risk. Not a good sign for equities.

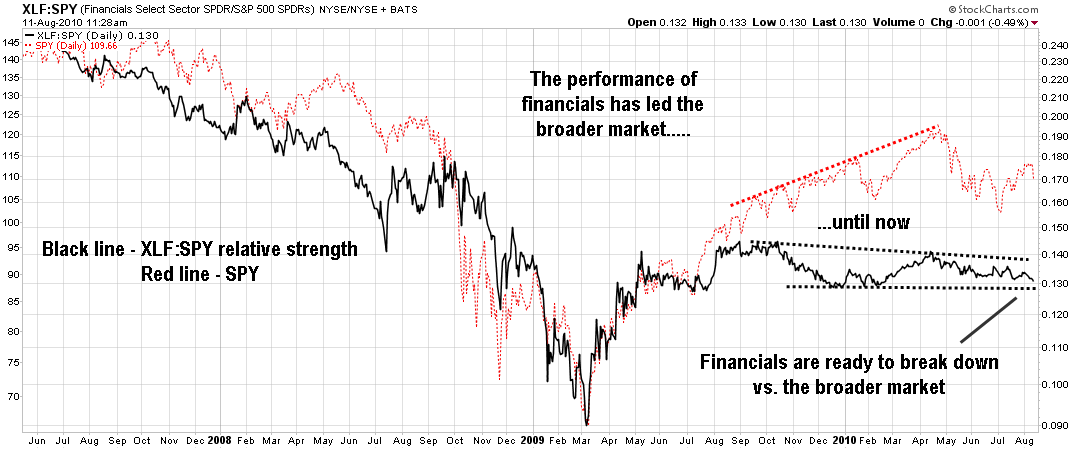

Finally, let's take a look at another key piece of evidence that shows this rally was built on a foundation of quicksand. The one sector that has been rather conspicuous in its lack of leadership during the last year has been the financials. Financials are vital to economic expansion as they are the conduits of capital to businesses and consumers. This sector has been the poster child of economic recovery aspirations, receiving a virtually endless supply of taxpayer money to prop up their poorly run institutions, yet they have woefully underperformed the broader market.

The chart below shows the relative strength between the financial sector ETF (XLF) and the broader market (SPY). When the black line is rising, financials are outperforming the broader market. When the black line is falling, financials are underperforming the broader market. The broader market (SPY) is the red line on the chart. Notice how the leadership of financials has been vital to market rallies in the past as the red and black lines rise and fall together - up until the fall of 2009. That is when the leadership of financial stocks disappeared. Again, more evidence that the recent rally has been running on fumes.

There have been warning signs all over this market for some time now and the lack of conviction on the part of buyers is now beginning to show. Ignore those that tell you now is the time to buy due to compelling 'valuations'. You will get a chance to buy at much, much better 'valuations' in the future (much lower prices).

댓글 없음:

댓글 쓰기